Of course recessions are always unexpected, aren’t they?

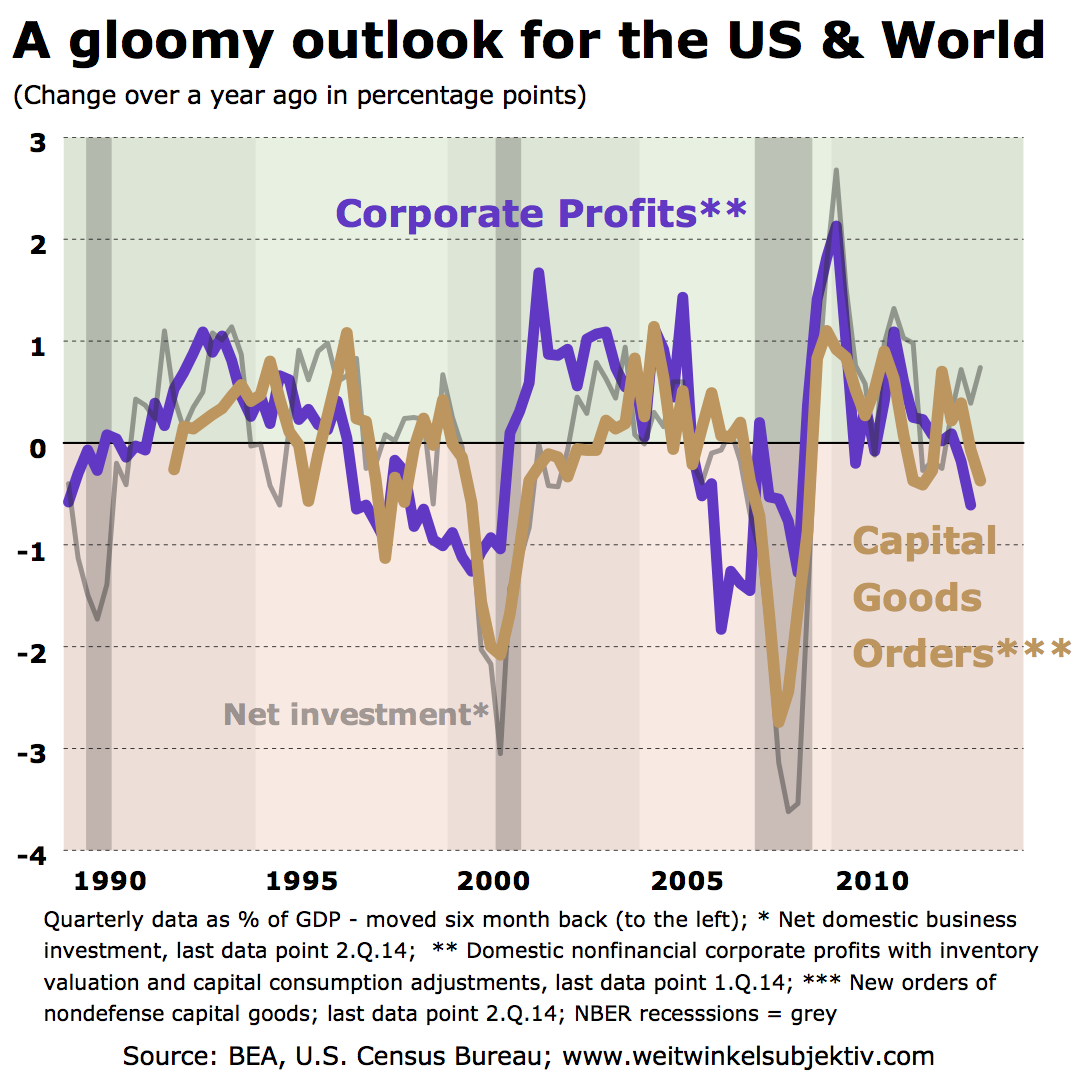

For those of you who believe American manufacturing is currently experiencing a healthy recovery and the Federal Reserve could raise their interest rates at any point soon – please take a look at this chart:

Usually profits always lead the business cycle, new orders for capital goods follow quickly and finally net investments run in the same direction. And if private net investments (as a share of income) turn negative (over a twelve months period) for a longer time, you can be quite sure that a recession begins within months. So it does not look good, neither for the US, Europe nor the global economy.

But who or what can save the US recovery now?: A stock market boom, China’s current account surpluses, massive new spending in construction or the Federal Reserve again? It is hard to see how this can happen now. In a previous post I described (in German) all the background. At this point I only like to quote the SocGen strategist Albert Edwards from his recent reports:

„In particular we have shown previously that the BEA’s whole economy profits series tends to lead both stockmarket measures of profits as well as the business investment cycle (…). In that sense monitoring whole economy profits can give a good indication of economic vulnerability and predict unexpected recessions (of course recessions are always unexpected!)”.